Big picture – Single-family vs last month & last year

-

Activity was solid, not crazy.

High-volume SF markets in November were:-

Newton (45 sales)

-

Lynn (33)

-

Quincy (33)

-

Beverly (21)

-

Peabody (19)

-

Lexington (19)

-

Plus a strong cluster in Needham, Malden, Saugus, Arlington, Dedham, Waltham, Milton, Salem, West Roxbury (11–18 sales each).

-

-

Prices are holding or drifting up per square foot, even where average sale prices look softer:

-

Many towns show YoY price-per-sqft increases (Belmont, Concord, Lexington, Newton, Lynn, Needham, Wellesley, etc.).

-

But average prices are often down vs last year in higher-end towns, suggesting smaller / more modest homes in the mix, not a collapse in values.

-

-

Competition is lower than peak-pandemic but still real.

In most reliable markets, sale-to-list ratios run around 99–102%, i.e. very close to asking, but the big over-ask blowouts (105%+) are rarer. -

Days to offer have lengthened almost everywhere vs last November:

-

Many towns are now in the 15–35 day range instead of low-teens or single digits.

-

That’s still a seller-friendly market, just not a frenzy.

-

(Note: wherever November had fewer than 8 sales, I treat the numbers as “thin data” and avoid strong claims.)

High-activity single-family markets to watch

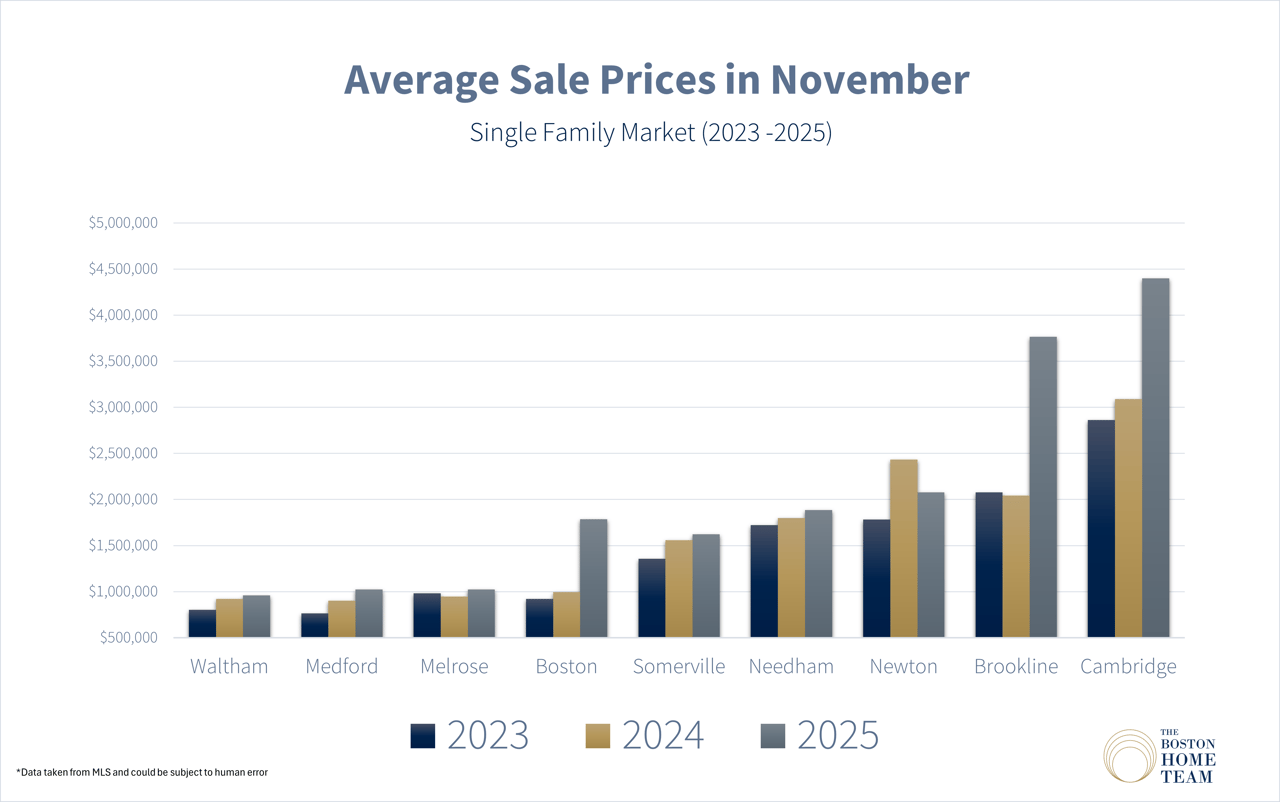

Newton – still the workhorse

-

45 sales in Nov (down slightly vs Oct’s 49, but up vs 37 a year ago).

-

Average price: ≈ $2.08M

-

Up ~20% vs Oct, but down ~15% vs last November (heavier mix of ultra-high-end closings last year).

-

-

Price per sq ft: ≈ $623, up vs both Oct and last year.

-

Days to offer: ~30 days, slower than last year (26 days).

-

Sale/list: ~97.8%, down from 101%+ last year.

Story: Newton SF is busy and expensive, with buyers taking more time and less willing to bid way over asking, but still paying more per foot than a year ago.

Lexington, Wellesley, Needham – high-end suburbs

Lexington (19 sales, solid sample)

-

Avg price ≈ $2.37M, up ~18% MoM and ~32% YoY.

-

PPSF ≈ $550, essentially flat YoY.

-

DOM up into the high-30s (was mid-20s last year).

-

Sale/list about 101% (still over-ask, but less wild than during 2022–23).

Wellesley (18 sales)

-

Avg price ≈ $2.33M, down modestly vs Oct and vs last year.

-

PPSF ≈ $690, up vs both periods – again, mix vs value.

-

DOM around 24–25 days, similar to last year.

-

Sale/list hugging 100%.

Needham (16 sales)

-

Avg price ≈ $1.89M, up mid-single digits vs both Oct and last year.

-

PPSF (~$561) is up strongly vs Oct and slightly vs last year.

-

DOM has stretched to about 32 days (vs ~18 a year ago).

-

Sale/list still around 101%.

Takeaway: the Route 128 luxury belt is price-resilient (especially per square foot) but clearly less frantic: homes are sitting longer and buyers have marginally more leverage.

North Shore & near-North – busy and more price-sensitive

Lynn (33 sales)

-

Strong activity: 33 sales vs 27 last year.

-

Avg price ~$612K (down ~5% YoY), but PPSF (~$420) is up ~12% YoY.

-

DOM ~20 days, double last year’s pace, and sale/list (~101%) has come down from 105%+.

Beverly (21 sales)

-

Avg price ≈ $979K, up ~13% vs Oct and ~23% vs last year.

-

PPSF is down vs Oct and a bit under last year – again pointing to bigger houses in the mix.

-

DOM around 17 days, very quick.

-

Sale/list a touch over 101%.

Peabody (19 sales)

-

Avg price ≈ $716K, essentially flat vs Oct and up ~7% YoY.

-

PPSF (~$375) is down vs last year, implying more space per dollar.

-

DOM in the high-teens, with sale/list just above 101%.

Salem (12 sales)

-

Avg price ~$761K (flat vs last year).

-

PPSF (~$423) up ~7% YoY.

-

DOM is longish at ~38–39 days, and sale/list around 101%.

Saugus (15 sales)

-

Avg price ~$686K, down vs Oct but up vs last year.

-

PPSF mid-$380s, a bit above last year.

-

DOM just under 20 days, sale/list ≈ 101.5%.

Takeaway: the North Shore SF market is active and generally competitive, but with slower absorption and more nuanced pricing: some buyers are getting more house for the money even as $/sqft remains firm or drifts up.

Inner-ring, mid-price suburbs

Arlington (20 sales)

-

Avg price ≈ $1.35M, up ~7% MoM and ~3–4% YoY.

-

PPSF (~$573) is down vs both Oct and last year, suggesting larger or less-renovated homes trading.

-

DOM jumped to ~36 days (was ~21 in Oct and ~10 a year ago).

-

Sale/list slipped from huge over-ask (107% last year) to essentially at asking (~100%).

Medford (11 sales)

-

Avg price ≈ $1.02M, up vs both Oct and last year.

-

PPSF (~$505) slightly down vs last year.

-

DOM ~14 days, much quicker than Oct’s almost-month-long average.

-

Sale/list about 100%.

Malden (15 sales)

-

Avg price ≈ $749K, up vs both Oct and last year.

-

PPSF (~$465) flat YoY.

-

DOM ~17 days, similar to last year.

-

Sale/list robust at ~104%.

Dedham (16 sales)

-

Avg price ≈ $893K, down vs both Oct and last year.

-

PPSF has eased, DOM has stretched into the mid-40s, and sale/list has drifted just under 100%.

Waltham (14 sales)

-

Avg price ≈ $958K, up modestly vs Oct and last year.

-

PPSF (~$453) has softened vs last year.

-

DOM in the high-teens, sale/list around 102%.

Takeaway: inner-ring SF markets are still very saleable, but:

-

Over-ask bidding is more selective, and

-

Days to offer are up compared with last November, especially in places like Arlington and Dedham.

Boston single-family neighborhoods (directional read)

Only a few Boston neighborhoods had enough SF sales in November to treat as reliable:

-

Dorchester (12 sales) – Avg ≈ $905K; PPSF has dropped vs last year, but prices are up ~25% YoY and DOM is now around 2 weeks. Sale/list around 98.5%, down from over-ask levels last year.

-

Jamaica Plain (9 sales) – Avg ≈ $1.67M, up ~21% YoY, with PPSF in the low-$600s and DOM in the mid-teens. Sale/list just under 98%.

-

Lynn-like outer Boston markets: Hyde Park, Mattapan, Roslindale, West Roxbury, Eastie, Charlestown, etc.

Most of these had fewer than 8 sales each, so month-to-month swings are mostly about which houses sold, not fundamental shifts.

Big picture in Boston SF:

Single-family homes in city neighborhoods are highly segmented and often driven by just a handful of trades. Where volume is decent (Dorchester, JP, West Roxbury), you see higher prices than last year but much tamer bidding.

Quick SF vs condo snapshots (same towns)

A few useful talking points where you have both product types:

-

Newton:

-

SF: 45 sales, ≈ $2.08M, ~$623/sqft, 30 days, 97.8% of list.

-

Condo: 27 sales, ≈ $1.08M, ~$590/sqft, 44 days, ~99% of list.

👉 SF is much more expensive and sells faster, but condos are currently closer to asking on average.

-

-

Cambridge: (thin SF sample – 7 sales)

-

SF: ≈ $4.4M, ~$1,083/sqft, 12 days, ~104% of list.

-

Condo: ≈ $1.38M, ~$1,013/sqft, 38 days, ~99% of list.

👉 The SF segment is a tiny, ultra-luxury niche that still behaves like a bidding-war market.

-

-

Somerville: (SF thin – 5 sales)

-

SF: ≈ $1.62M, ~$734/sqft, ~12 days, ~102% of list.

-

Condo: ≈ $929K, ~$746/sqft, ~21 days, ~100% of list.

👉 Condos dominate volume; SF is a low-inventory, high-price add-on.

-

-

Quincy:

-

SF: 33 sales, ≈ $876K, ~$456/sqft, 25 days, ~100% of list.

-

Condo: 21 sales, ≈ $574K, ~$488/sqft, 26 days, ~99% of list.

👉 SF and condos move at similar speeds, but condos get a slight $/sqft premium; SF is the bigger ticket.

-

-

Salem:

-

SF: 12 sales, ≈ $761K, ~$423/sqft, 39 days, ~101% of list.

-

Condo: 21 sales, ≈ $578K, ~$439/sqft, 38 days, ~97% of list.

👉 SF buyers in Salem are still bidding over ask, while condo buyers have a bit more negotiating room.

-