The Spring That Split in Two

Four months into the 2026 spring selling season, the pattern is clear. Single-families fell. Condos held. Multi-family quietly moved. This isn’t one market story — it’s three, running simultaneously across the same geography.

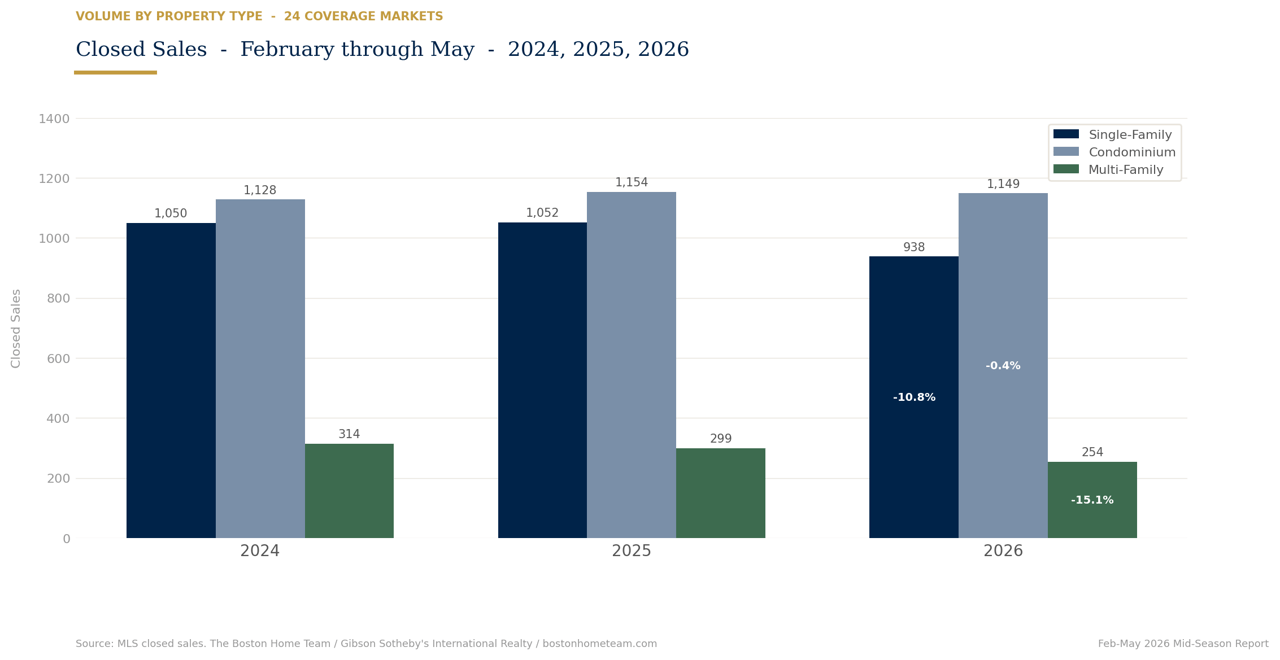

The two-track story that defined late 2025 is now an established pattern. Across 24 coverage markets — from Jamaica Plain and Cambridge through the North Shore — single-family volume has fallen roughly 11% year over year through May, and the decline holds almost identically against 2024 (-10.7%). This is not a one-year wobble. It’s a two-year compression of SF transaction activity that’s showing no sign of reversal in the February–May data.

Condos are the counterweight. 1,149 CC transactions across coverage markets through May, essentially flat year over year and slightly above 2024 levels. In the markets where SF demand has dried up, condo volume has often expanded — buyers adjusting to price reality rather than exiting entirely. Multi-family is falling from a different angle: rate sensitivity among investor-buyers and tighter lending are compressing MF activity at a steeper rate than even SF.

The divergence is not uniform. Several coverage markets are outperforming sharply. A few have broken down across all three metrics simultaneously. And one market — Hyde Park — is doing something that no other primary coverage market is doing through the first four months of the selling season.

24 coverage markets · February–May 2024–2026

−10.7% vs ’24

+1.9% vs ’24

−19.1% vs ’24

Four markets that broke from the pattern

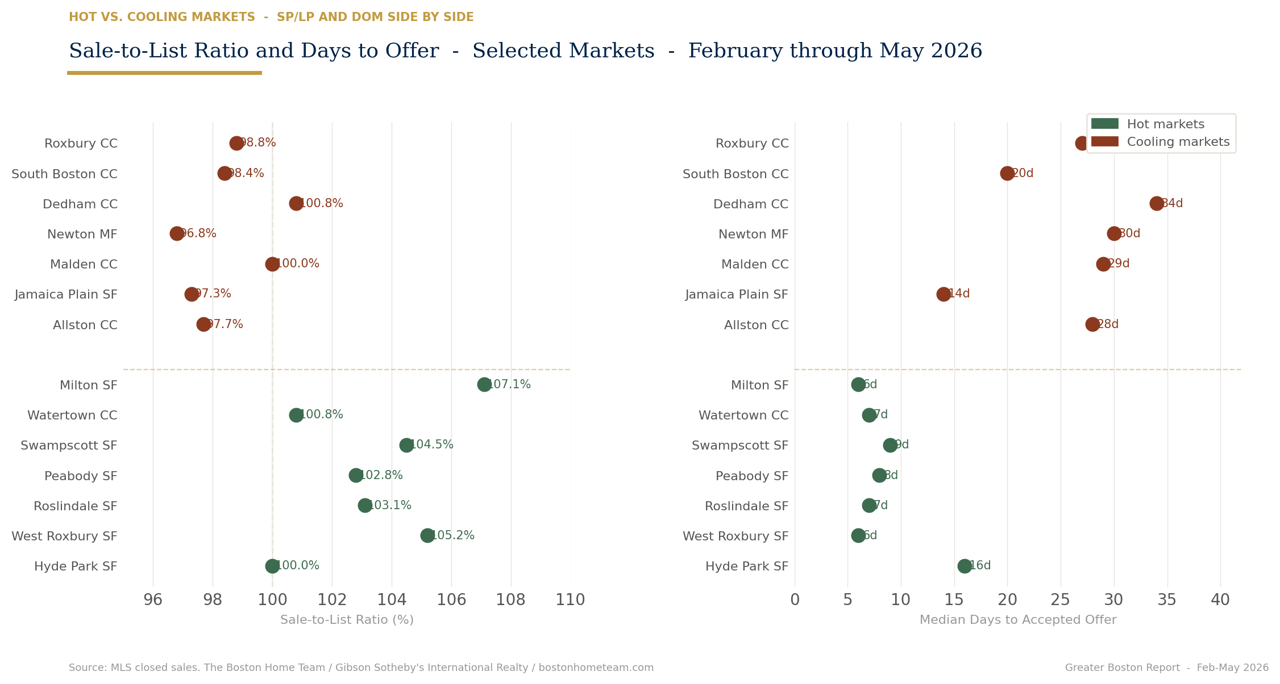

Markets with 15+ sales · Feb–May 2026

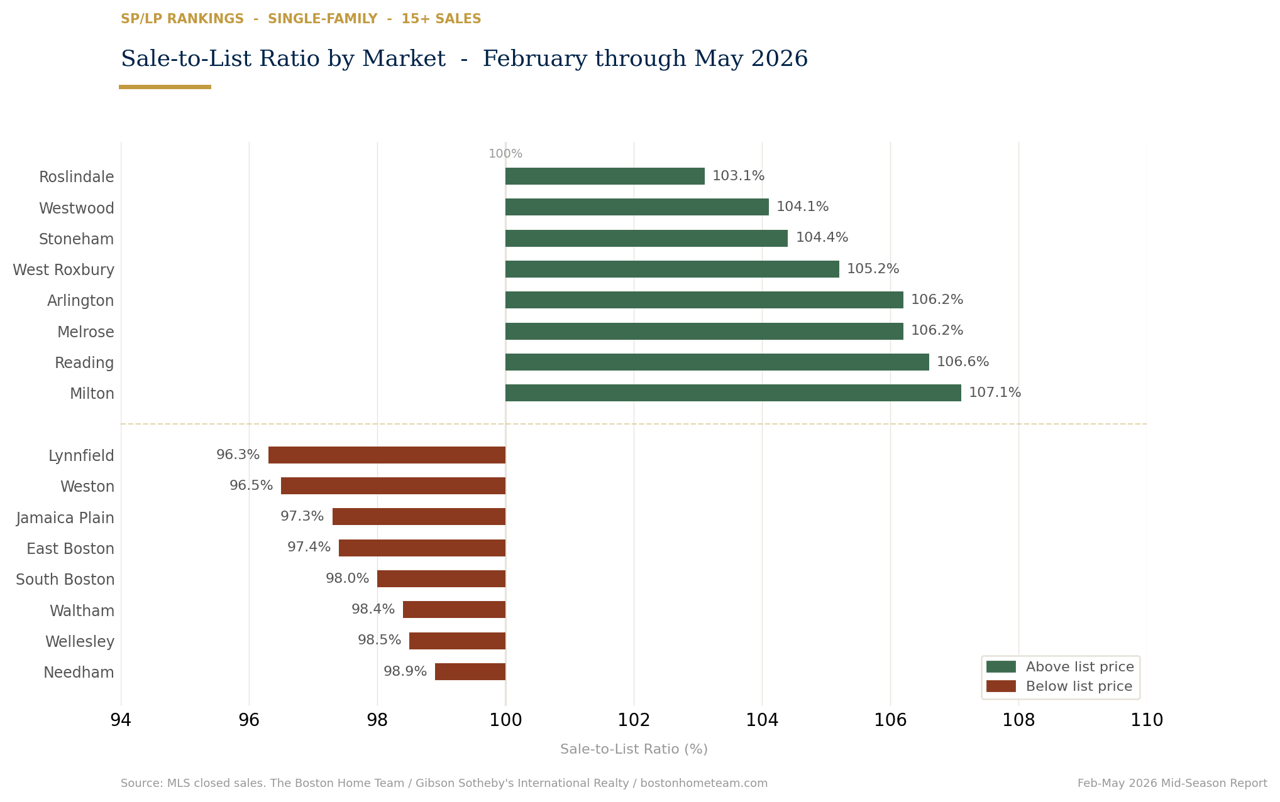

Highest Sale-to-List

#1Milton

107.1%

#2Reading

106.6%

#3Melrose

106.2%

#4Arlington

106.2%

#5West Roxbury

105.2%

#6Stoneham

104.4%

#7Westwood

104.1%

#8Roslindale

103.1%

Lowest Sale-to-List

Lynnfield

96.3%

Weston

96.5%

Jamaica Plain

97.3%

East Boston

97.4%

South Boston

98.0%

Waltham

98.4%

Wellesley

98.5%

Needham

98.9%

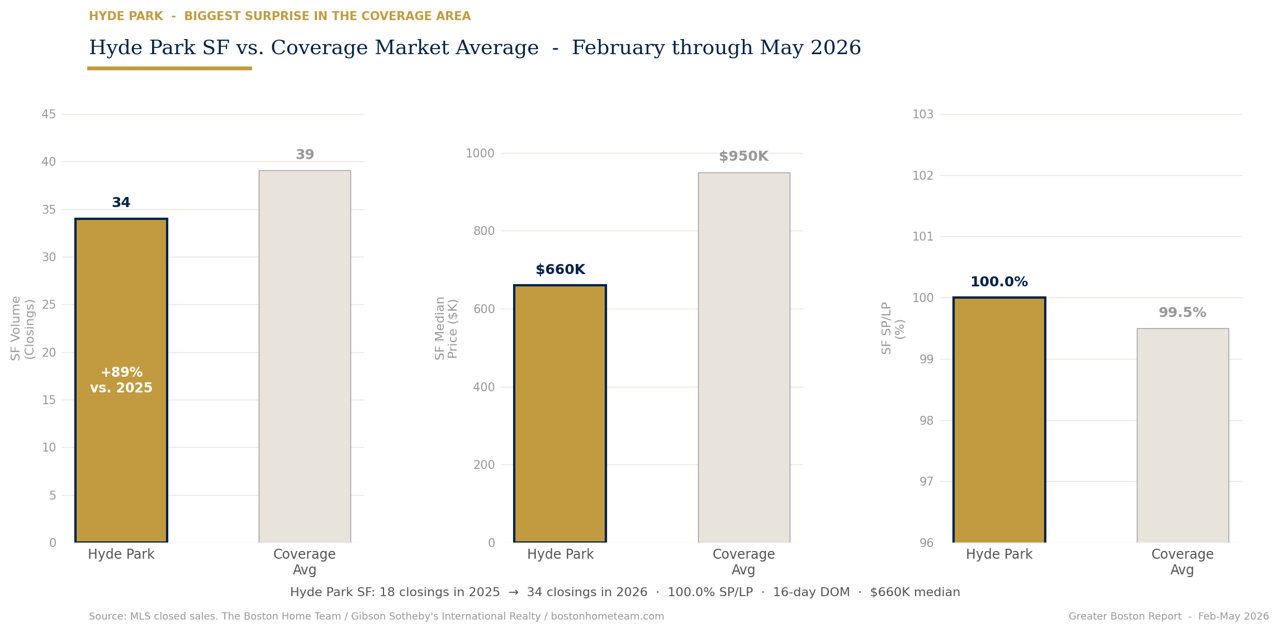

Six-day median DOM. $1.2M median price. A mix-effect caveat applies to the YoY price jump, but the competitive pressure is real: Milton SF buyers are paying over ask quickly, and have been for two straight years.

Markets moving sharply in either direction

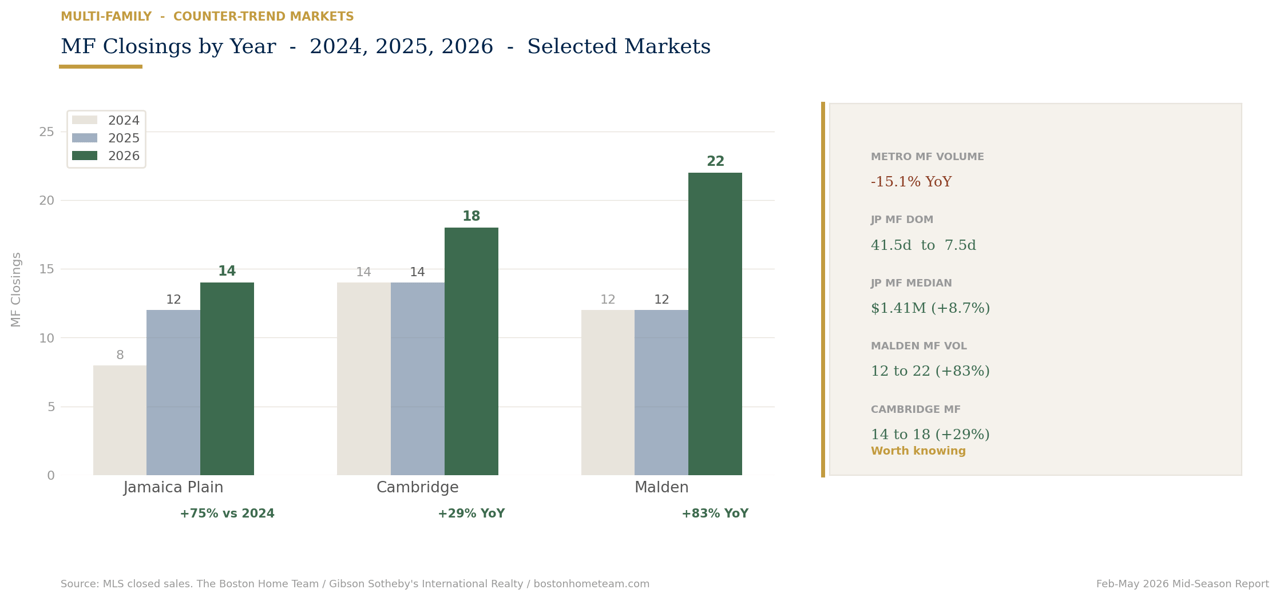

The stealth story inside a declining headline number

The multi-family headline at the metro level is declining volume — down 15% across coverage markets. But within that decline, a handful of specific markets are quietly running counter-trend, with MF volume and pricing that tell a different story than the SF data in the same zip codes.

8 → 14 closings · $1.41M med

14 → 18 closings · $2.1M med

12 → 22 closings · $995K med

The JP multi-family resurgence is the most notable in the corridor. MF volume has more than doubled from its 2024 base (8 → 14 closings through May), DOM has tightened dramatically (41.5 days in 2024 to 7.5 days now), and median price is $1.41M — up 8.7% year over year. This is a market segment that was struggling two years ago and has found its footing, driven in part by buyers seeking owner-occupied two-families as an alternative to the softening SF market at similar price points.

Malden’s MF surge (12 → 22 closings, +83%) and Cambridge MF growth (+29%) both confirm the pattern: in higher-cost markets where buyer purchasing power has been stretched, the two-to-four family is serving as a creative entry point for buyers who can offset mortgage costs with rental income.

A market reorganization, not a market downturn

“In the markets where SF demand has dried up, condo volume has often expanded — buyers adjusting to price reality rather than exiting entirely.”

This report covers 24 Greater Boston markets — including Jamaica Plain, West Roxbury, Hyde Park, Roslindale, Allston, South Boston, East Boston, Cambridge, Watertown, Milton, Newton, Needham, Wellesley, Westwood, Waltham, Dedham, Malden, Medford, Arlington, Reading, Melrose, Stoneham, Swampscott, Peabody, and Lynnfield — using closed MLS sales data from February through May 2026, compared against the same period in 2025 and 2024. Markets with fewer than 5 transactions in any period are excluded from trend analysis. This report is part of an ongoing series tracking real estate conditions across Greater Boston published each season by The Boston Home Team at Gibson Sotheby’s International Realty. BJ Ray has tracked Greater Boston real estate data across these markets for 21 years.

24 markets. Three property types. One team that tracks all of it. If you’re trying to understand what the spring 2026 data means for your specific situation — buying, selling, or deciding whether to move at all — that’s the conversation we’re built for.